To serve you better, our new website displays information specific to your location.

Please visit the site and bookmark it for future use.

Complexities in Mineral Project Evaluation

Preparing a cash flow model to be used in project evaluation is not just an exercise in manipulating numbers in Microsoft Excel. There are numerous complexities in compiling such a model which require a thorough understanding of the project and the commodity, from geology to mining to processing to logistics to marketing the finished product. There are technical matters specific to product and commodity to be considered. Further, the terms of any off-take / marketing agreement or toll-treating agreement need to be used accurately and properly modelled.

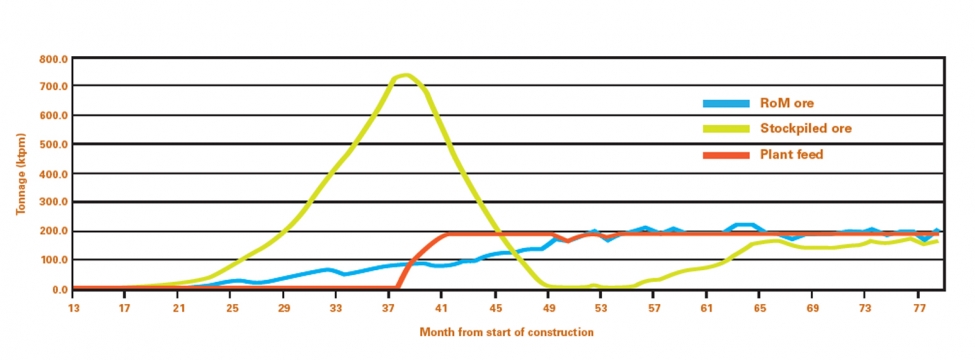

In most projects, month zero (marking the start of the project) is not the same for the mining and the processing components. The mining ramp-up to steady state invariably takes much longer than that of the processing plant (see diagram). The time when the first ore can be fed into the plant needs to be carefully assessed, so the size of the run-of-mine (RoM) stockpile during construction does not get too large, compared to a plant that is brought on stream too early -- only to be starved of RoM ore (reducing revenue and increasing unit costs).

This requires carefully modelling the movements of tonnages and contained metal into and out of the stockpile.

A simple error is the incorrect use of terminology with respect to processing plants: with coal, industrial minerals and dimension stone, apply yield to RoM tonnage to describe the percentage of saleable product to be derived; with precious and base metals, apply recovery as a percentage of contained metal in the plant feed. With projects such as platinum group metals (PGMs), relationships exist between the head grade of the plant feed and the applicable recovery – the higher the grade, the higher the recovery. A further complication is that the distribution of the PGMs in the plant feed, or the prill split, varies from project to project, and the recoveries that apply to the various elements are different. Applying an average recovery tends to understate the recovery of the main revenue drivers, platinum and palladium, and overstate the Au (gold) recovered, with a general reduction in revenue.

This discussion introduces a few of the many important distinctions in calculating elements that can impact cost estimates and make the difference between success and failure.

For instance: were capital cost estimates phased independently for each component? How were costs determined? Who has considered the effects of changing foreign exchange rates? Does the mining licence grant ownership of the surface? How about funding for the environmental closure costs? Are the evaluation models calculated in real or nominal terms? And what about inflationary effects?

The SRK study team looks closely at all of these eventualities, critically reviewing and validating them against historical operating statistics.

Andrew McDonald: amcdonald@srk.co.za

|

You can download a PDF of the entire |

PDF

A4 |

PDF

Letter |

|

|

|

Our newsletters focus on specific areas of interest to earth resource professionals and clients. Each is available as an Adobe Acrobat PDF file. If you don't already have Adobe's PDF reader, you can download it free.

![]()